Centrelink Rule Changes for Account Based Pensions!

As part of the ongoing Centrelink and superannuation reforms, the Government has extended the Centrelink deeming rules to superannuation account based pensions commencing after 1st January 2015. This means that account based pensions will be treated as a financial asset and deemed under the income test. If you already have an existing account based pension, then this won’t apply to you unless you change product providers any time after next year.

So what does this mean exactly?

To gain a better understanding of the rules changes, you firstly need to know what the deeming rules are. Deeming rules assume your financial assets are earning a certain amount of income, regardless of the income they actually earn. Deeming is used to calculate income for government pensions, benefits and allowance payments.

If you’re in receipt of a Centrelink income support payment or are likely to eligible for one in the near future, and you have funds within your superannuation, now is a good time to consider commencing an account-based pension prior to the rule changes on the 1st January 2015. This is to take advantage of the grandfathering provisions to avoid being faced with a potential decrease on your government benefits, in particular the Age Pension.

Current Situation

Currently, the income counted towards Centrelink’s income test from your account-based pension is the pension payments you receive for the year less a deductible amount. This usually results in a very low amount being considered as income for Centrelink purposes. The introduction of deeming on superannuation account based pensions (previously known as allocated pensions) may disadvantage pensioners as the deemed income is likely to be greater than the current treatment, which may result in a reduction of the Age Pension payment.

After 1st January 2015

From 1 January 2015, all new account based pensions will be deemed as earning a certain rate of income regardless of the actual return of the investment. The deeming rates listed below are applied to the total market value of all of your financial investments.

The new deeming rules will not apply to:

- Defined Benefit Pensions.

- Lifetime and Life Expectancy Annuities.

- Fixed Term Annuities if the term is longer than five years.

How does this change affect existing income support recipients?

If you’re already receiving income support (such as the Age Pension) from Centrelink and you have commenced, or will commence, an account based pension prior to 1 January 2015, you will not be impacted by this change. However, changing from one product provider to another after 1 January 2015 will result in you being caught by the change in rules.

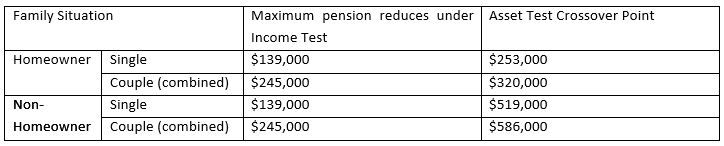

Pensioners commencing the account based pension after the 1st January 2015 would be assessed based on both the asset and income tests. The test which gives a lower entitlement would be applied towards the government benefit.

As shown in the table above, a single homeowner with financial investments below $139,000 and no other income or assets will be entitled to the full Age Pension and will not be affected by these changes.

If the value of a pensioner’s financial investments lies between $139,000 and $253,000, their pension entitlement will be determined by the Income test. These pensioners will be affected by the new deeming changes, as the additional assessable income will reduce their Age Pension entitlement. Pensioners with assets above $253,000 will be assessed under the Assets Test instead of the Income Test, and will not be impacted by the changes.

If your investments (including super) are between $139,000 and $253,000, and you’re currently receiving the Age Pension, or will be eligible for the Age Pension before the 1st January, the time to review your financial situation is now. Having an account based pensions in place before 1st January 2015 will qualify for grandfathering provisions and you’ll continue to be subject under the current rules as long as you’re in receipt of an eligible Centrelink Income Support Payment.

Please feel free to call our office on (02) 8776 0104 if you require further information on this topic.

Follow Us!

|

|

|